Business credit vs. personal credit: What sets them apart?

To protect your personal assets and build a strong financial profile for your company, you need to understand the distinction between business credit vs. personal credit. Business credit is the capital your company borrows for growth, while personal credit is the capital you borrow as an individual.

In this article, we’ll show you why you should build a solid standalone business credit profile and how it unlocks access to flexible capital that can move your business forward.

Benefits of building strong business credit

Many companies start off relying on their owners’ personal savings to cover business expenses. That approach isn’t sustainable for getting your business ready for significant growth.

A strong business credit profile allows you to secure funding based on your business’s future potential and not the value of your personal assets. To put it in perspective, your personal credit might get you $50K, but your business credit could qualify you for $10M.

There are three other major advantages a strong business credit profile offers:

- Higher credit limits: Access to more capital means you can fund transformative projects like acquiring a smaller competitor, automating your production line, or opening a new national distribution center.

- Lower financing costs: A strong business credit profile means you’re more likely to pay interest at lower rates. Every dollar you borrow works harder for you, improving your net margins and flowing back to your bottom line.

- Greater flexibility: You can move faster to take advantage of opportunities when they appear, like buying inventory in bulk at a deep discount. Lenders and suppliers see you as a credible, low-risk partner, so they’re able to turn around applications faster and offer you great terms.

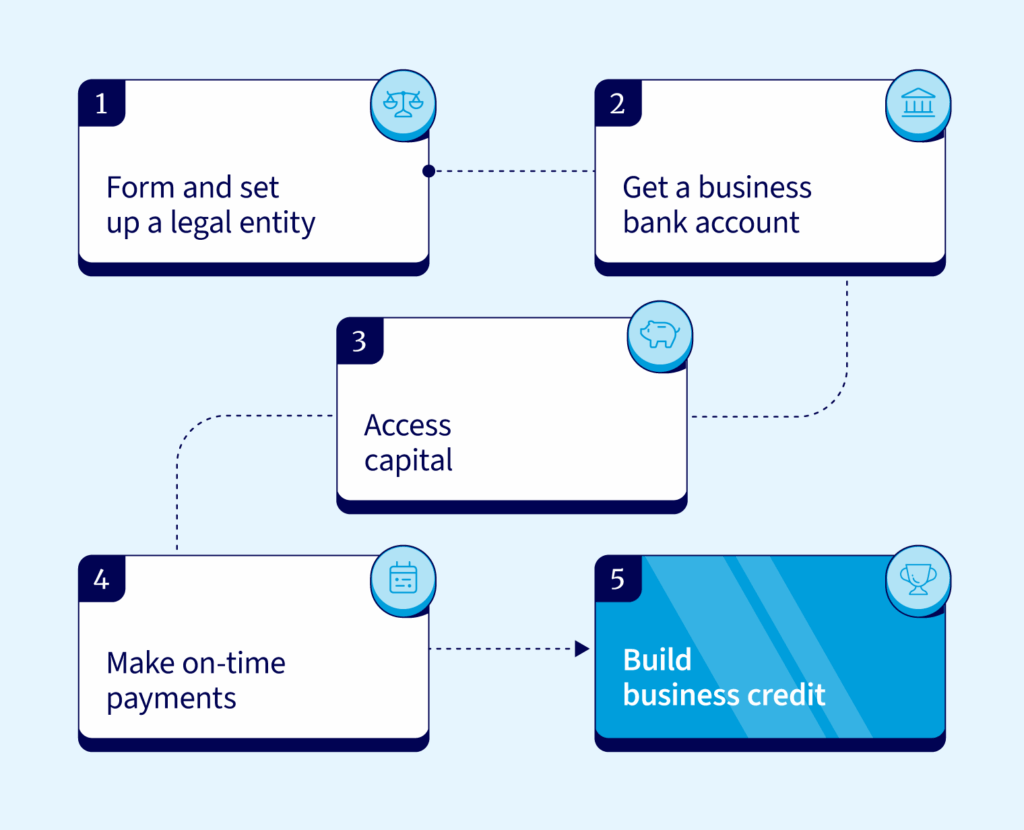

How to build strong business credit

To secure the funding you need to power company growth, take the following five steps to build a strong business credit profile:

- Establish a separate legal entity: Registering as an LLC or an S-Corporation differentiates you from your business. This allows the company to build its own credit history.

- Set up a D&B file: D&B is a primary source of data for commercial lenders. Apply for a free D-U-N-S Number to open a credit file and make your business visible to more lenders and suppliers.

- Open a business bank account: Run all company income and expenses through a dedicated business account. This creates a clear financial trail and shows lenders you manage your finances well.

- Apply for credit: Use a business credit card for regular company spending and pay it off on time. Do the same with any suppliers that offer business tradelines and report payment performance to the business credit bureaus. Both types of payment activity help build your business credit history.

- Pay bills on time: On-time payments are the most important part of your business credit score. They prove your business’s financial health and show lenders and suppliers that they can trust you to meet your obligations.

Building a strong business credit profile takes time and patience. You can typically establish your initial credit file within 30-60 days of completing these steps, but developing a meaningful credit history requires 6-12 months of consistent payment activity.

The strongest business credit profiles – those that unlock the best financing terms and highest credit limits – usually take 12-24 months to develop. Starting early with even small credit amounts is crucial, as lenders and suppliers value consistent payment patterns over time more than the size of individual transactions.

Business credit vs personal credit: What’s the difference?

The main difference between business credit and personal credit is:

- Business credit is capital you use to invest in your company; for example, buying inventory in bulk, funding a major marketing campaign, and launching a new product line. It’s important to keep this separate to build a strong, independent credit profile for your business. This is set up by obtaining credit cards and loans in your business’s name and EIN, not your personal name.

- Personal credit is capital you spend on yourself and your family; for example, buying a family car, funding a vacation, and paying for a wedding. Mixing this with business expenses can jeopardize your personal financial health. A clean separation is achieved by ensuring all personal spending uses accounts tied only to your individual Social Security Number and personal credit history.

There are other important differences, too, starting with the credit scoring system.

Scoring system

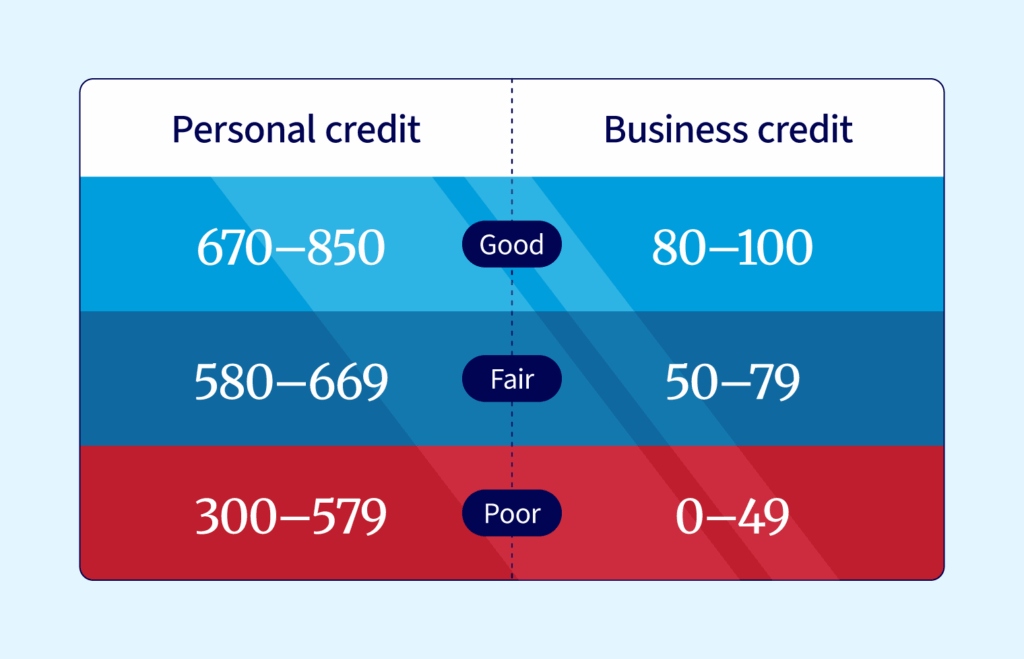

Personal FICO® credit scores range from 300 to 850. The higher the score, the stronger your profile is as a borrower.

Business credit scores rate your company on a scale of 0 to 100, based on your payment history with suppliers, vendors, and lenders.

A strong business score of 80 or above means you’re seen as a responsible borrower, which makes you more likely to be accepted for larger credit facilities and lower interest rates.

Credit limits

Businesses can borrow far more than individuals for one simple reason: businesses borrow to invest while people borrow to consume.

For example, a person might finance an SUV for $50,000. From a financial point of view, the SUV generates no capital and reduces the person’s discretionary income through monthly loan repayments.

A New York-based last-mile delivery company, in contrast, might borrow $2M to buy a fleet of vans. Each vehicle generates revenue for your business, ideally more than its financing costs. A van with a $1,000 a month payment might generate an extra $3,000 in monthly net profit.

This is the main reason businesses can borrow more. They use the capital to purchase assets that pay for themselves and fuel future growth.

How the credit is used

You can see how consumers and businesses use finance differently by the different types of loans offered.

These are common examples of how consumers use personal credit:

| Type of finance | Typical use case |

| Personal credit card | People use personal credit cards to pay for everyday purchases and manage short-term expenses. |

| Auto loan | Auto loans finance the purchase of personal vehicles. |

| Personal loan | Consumers often use personal loans to cover the cost of one-time expenses like home improvement or a wedding. |

| Student loan | Student loans cover expenses like tuition fees and other costs for higher education. |

| Vacation loan | This provides consumers with the funds they need to pay for a vacation when their personal finances won’t stretch to the cost. |

In comparison, business loans target a return on investment, like these examples:

| Type of finance | Typical use case |

| Large business loans | Businesses use large business loans to invest in growth by meeting the costs of expansion or acquiring a competitor. |

| Business line of credit | Business lines of credit provide companies with flexible capital for managing day-to-day cash flow and seizing unexpected opportunities. |

| Equipment financing | Businesses use equipment financing to purchase specific, income-generating assets like machinery or vehicles. |

| Invoice factoring | Factoring unlocks working capital tied up in unpaid invoices and can help preserve working capital. |

| Inventory financing | Inventory financing provides companies with the capital they need to purchase inventory without depleting their operational reserves. |

Reporting agencies

Consumer credit bureaus like Equifax and TransUnion track your personal payment history. Business credit bureaus like Dun & Bradstreet (D&B) track the payments you make to suppliers, vendors, and lenders.

Legal responsibility

With personal credit, you’re responsible for all debts registered in your name. If you miss payment dates or your account goes into default, your personal credit score will take a significant hit, making it a lot harder to borrow in the future.

When your business is registered as a separate legal entity, like an LLC or corporation, it becomes responsible for its own debts.

However, because of that separation, lenders often require you to sign a personal guarantee. This is when you agree to repay the outstanding balance personally on a finance facility your company takes out.

In some cases, lenders might also ask for collateral. Collateral is a specific business asset, such as equipment or inventory, that you pledge as security for the financing. If you don’t keep up with repayments on the loan, the lender can recover the asset to help cover the outstanding debt.

Why it’s important to separate business and personal credit

Establishing a distinct financial and legal identity is often the first strategic step in moving a business forward. It enables you to go beyond using your personal credit cards and take advantage of business financing solutions to grow and scale.

Four important benefits include:

- Protects personal assets with a legal firewall: Using business credit establishes a clear, legal separation. It ensures that business debts and liabilities remain with the company, shielding your personal assets, like your home and personal savings, from business-related lawsuits or vendor disputes. While personal guarantees may be required for some loans, this separation limits your exposure and protects everything else.

- Builds a strong, independent business credit profile: Relying on personal credit for business needs prevents you from establishing a standalone business credit history. Using dedicated business credit products is the only way to build a strong business credit score, which is essential for unlocking higher funding limits and better loan terms based on your company’s financial health, not your personal finances.

- Creates transparency for lenders and investors: Mingling personal and business credit can be a major red flag for banks and investors. It makes assessing your company’s true financial health nearly impossible, branding you as high-risk. A separate business credit history provides a clear, verifiable picture of your company’s performance and debt management, making it significantly easier to secure funding and attract partners.

- Increases business value and sale potential: When it’s time to sell, potential buyers conduct thorough due diligence. A history of using business credit (instead of personal cards or loans) provides a clean, auditable trail that proves your company’s profitability and financial responsibility on its own merits. This standalone financial story makes your business a more valuable and sellable asset.

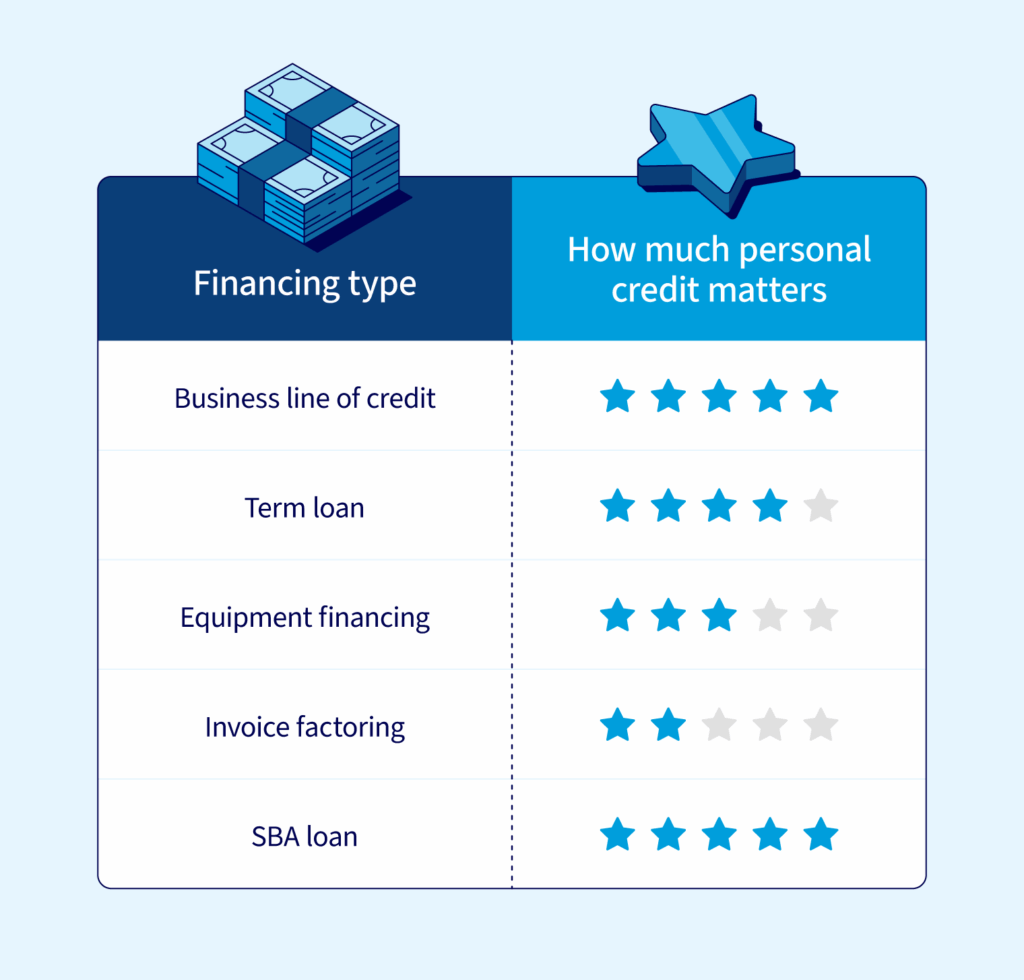

How personal credit affects business financing

Although your business credit score is more important, your personal credit score still counts. That’s especially true for younger businesses with limited credit histories. In these cases, lenders often use your personal score to assess how financially disciplined you are.

How much your personal credit matters depends on the type of funding you apply for, as you can see from this table:

Find financing that supports your business goals

Separating personal finances from business finances is an important step every business has to take to grow. Understanding the business credit vs. personal credit difference is the first step to building an independent financial identity for your company. A strong independent business credit profile opens the door to the flexible financing you need to fuel your growth. National Business Capital’s expert advisors help you find the right funding option to move your business forward, from term loans that fund your next expansion project to purchase order financing so you can fulfill large customer orders without affecting your working capital. Apply today to find out what’s available to you.

Frequently asked questions

You need both, especially in the early days. In the long term, your priority should be building your business credit score. While a strong personal score shows you’re responsible with capital, a strong business score is what helps your company qualify for growth funding.

Lenders look first at your business credit score from bureaus like Dun and Bradstreet to assess the financial health of your business. If your business has a limited credit history, lenders may also review your personal FICO® score as a key indicator of your financial discipline.

Business loans can affect your personal credit. First, if you apply for a business loan, many lenders perform a hard personal credit check, which can cause a dip in your score.

Second, if you sign a personal guarantee, you make yourself personally liable for the debt. If the business then defaults on that loan, the lender can report the default on your personal credit history because of the guarantee. That reported default can severely impact your personal credit score.

ABOUT THE AUTHOR

Joseph Camberato

Founder & CEO

Joe Camberato is the CEO and Founder of National Business Capital. Beginning in 2007 out of a spare bedroom, Joe and his team have financed $2+ billion for businesses nationwide. He’s made it his calling to deliver the educational and financial resources businesses need to thrive.